Flood insurance

Are you paying the right price for flood?

Flood rating is all in the details. A few of them can move your premium significantly — here's what actually drives it.

Every flood quote starts at your elevation — never a generic rate.

Flood zones & pre/post-FIRM

Flood insurance uses many different pieces of information to generate a premium unique to the risk. It starts with the location address, which determines the property's flood zone. The risk is then classified as pre-FIRM or post-FIRM based on the year of original construction.

Foundation type matters too. A slab on grade, a crawl space, a basement, or a combination of these each affect the rating. Depending on the property, flood rates can be subsidized or actuarial.

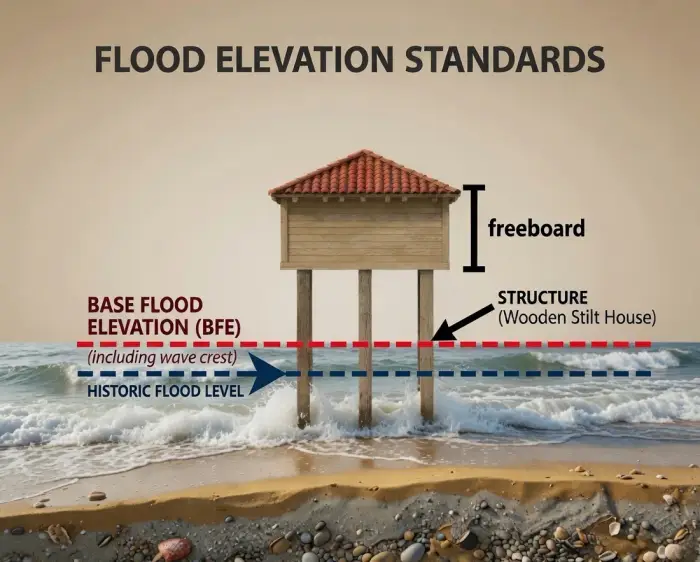

Elevation certificates

Since Super Storm Sandy in 2012, buildings elevated on an unfinished enclosure have become common. These enclosures are carefully designed to keep flood water away from the finished areas of a structure. A surveyor or engineer can determine a building's floor heights and record them on an elevation certificate, which may benefit a flood quote. Elevated buildings generally use flood vents — most often engineered vents — to equalize water pressure on the foundation during a flood.

What to bring for a quote

There's a lot to get right, and small differences change the number. If you have an elevation certificate, a prior flood declarations page, or a recent survey, bring those — we can help you navigate the flood insurance process from quoting all the way to policy issuance.

Why McLear

We check elevation before we quote

A foot of elevation can swing a flood premium. We pull your certificate, flood zone, and community rating so you pay for the risk you actually have.

- Elevation certificate review, included

- NFIP and private flood options compared side by side

- Community rating system discounts applied where earned

Next step

Ready for a flood quote?

Bring an elevation certificate if you have one — we'll handle the rest.